Introducing Principal PRS decumulation solution.

A happy retirement needs long-term planning for financial stability and security. As part of Principal Private Retirement Schemes (PRS) offering, PRS decumulation solution is a retirement solution that comes with Regular Withdrawal Plan (RWP) that lets you customise your post-retirement cash flow based on your goals and needs. Better still, you can continuously invest your remaining balance in the funds for potential returns, so that your next chapter in life can go even further.

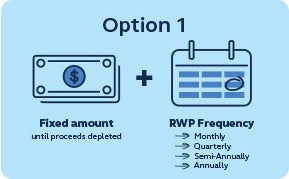

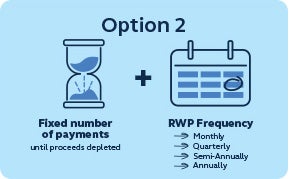

You can personalise your withdrawal schedule with RWP. There are 2 options available for your selection:

Why invest with Principal?

Principal RetireEasy Income and Principal Islamic RetireEasy Income fund work to your benefit:

- Choice of Conventional or Islamic funds with global exposure. You can select either the Principal RetireEasy Income or Principal Islamic RetireEasy Income.

- Regular Withdrawal Plan (RWP)* enables you to customise recurring withdrawals at your preferred amount and pace. You’ll receive automatic transfers of RWP proceeds to your bank account on schedule, for maximum convenience.

- Your remaining balances in the fund will continue to be invested for potential returns, so that you can go even further with a growing account balance.

- With the beneficiary nomination feature, you can make a nomination for the purpose of easy disbursement of your PRS balance in the event of your demise.

*Only investors 55 years old and above are eligible for RWP.

- You can enjoy personal tax relief for contribution of up to RM3,000** annually, equivalent of up to RM840 yearly relief in tax.

- The PRS incomes will be exempted from tax, including Foreign Source Income (FSI) tax.

- Managed by Principal, a global investment leader with more than 142 years of financial expertise spanning over US$990 billion# assets worldwide.

**For contributions into the PRS and deferred annuities effective from years of assessment 2012 to 2025.

#As of December 2021.

Not sure how to plan your retirement savings? You can leave your details and our Customer Care representative will be in touch with you soonest possible. Consider reaching out to a financial consultant? We can help you find one. They can help you discover your goals and advice you based on your risk tolerance.

Principal PRS decumulation solution FAQ

Everything you need to know about Principal PRS decumulation solution!

What is Principal PRS decumulation solution?

The Principal PRS decumulation solution - It enables you to customize your withdrawal and continue to grow your PRS for your post-retirement need. The Principal PRS decumulation solution comprises of 2 components:

- Regular Withdrawal Plan (RWP)

Let you custimise and schedule withdrawals based on your goals and cash flow needs.

- Funds

The Principal RetireEasy Income (REI) and Principal Islamic RetireEasy Income (iREI) helps you to continue grow your PRS balances, so that it an prolong the sustainability of your account balance after retirement.

How can the Principal PRS decumulation solution benefits you?

Regular Withdrawal Plan (RWP)

- Customization – You may customize and schedule the withdrawals based on your post-retirement cash flow need.

- Convenience – The withdrawal proceeds will be transferred automatically to your bank account.

- Ease of setting up – One-off application to schedule for multiple future withdrawals.

Principal RetireEasy Income or Principal Islamic RetireEasy Income (Funds)

- Dedicated funds designed to suit retiree’s need

- Help investor to continuously grow their remaining fund balance while they withdraw from the Funds to support post-retirement needs.

- Choice of conventional or Islamic funds

- Funds are unconstrained in asset allocation with global exposure

- Funds offer a controlled risk and return profile.

- Income earned by the Funds are tax exempted, including the Foreign Source Income (FSI) tax.

- Managed by Principal, a global investment and retirement leader with more than 142 years of financial expertise.

Additional benefits

- Tax benefit – You can enjoy personal tax relief of up to RM3,000 for contribution into PRS (effective from year of assessment 2012 to 2025).

- Nomination – You can make nomination for the purpose of easy disbursement of your PRS balance in the event of your demise.

What is the allocation asset of the Funds?

The Funds are unconstrained in terms of asset allocation and region exposure (i.e., no fixed allocation or weightage in underlying assets or country). The Funds are managed with strategic or long-term asset class targets and target ranges. There is a rebalancing strategy that aligns with the target weights to identify asset classes that are either overweight or underweight. The Fund may shift asset class targets in response to normal evaluative processes or changes in market forces or Fund circumstances.

For Principal RetireEasy Income:

Up to 100% of the Fund’s NAV may be invested in collective investment schemes (including exchange-traded funds (ETF) and real estate investment trusts (REITs), equities, debt securities, money market instruments and/or deposits. Notwithstanding,

- up to 40% of the Fund’s NAV may be invested in unrated debt securities; and

- up to 10% of the Fund’s NAV may be invested in unlisted securities.

For Principal Islamic RetireEasy Income:

Up to 100% of the Fund’s NAV may be invested in Islamic collective investment schemes (including Islamic exchange-traded funds (ETF) and Islamic real estate investment trusts (REITs), Shariah-compliant equities, Sukuk, Islamic money market instruments and/or Islamic deposits. Notwithstanding,

- up to 40% of the Fund’s NAV may be invested in Unrated Sukuk; and

- up to 10% of the Fund’s NAV may be invested in unlisted Shariah-compliant securities.

Currently, the Funds will seek exposure to the various asset classes by investing in CIS (including ETF and REITs) to achieve greater market exposure, diversification and for cost efficiency purposes. At any point in time in the future, the Funds may invest directly into the various asset classes it is deemed appropriate and at the Manager’s discretion.

What is Regular Withdrawal Plan (RWP)?

RWP allows Eligible Members to customize and schedule the withdrawal arrangement based on your post-retirement cash flow need. You may schedule to receive a pre-determined amount of withdrawal proceeds at your preferred frequency.

Disclaimer

Investing involves risk and cost. You should read the relevant Prospectus, and/or Disclosure Document including any supplemental thereof and the Product Highlight Sheet (if any) before Investing. You should understand the risks involved, compare and consider the fees, charges and costs involved, make your own risk assessment and seek professional advice, where necessary. Securities Commission Malaysia does not review advertisements produced by Principal. For full disclaimer, please visit bit.ly/Principal-PRS-Disclaimer