10 min read I Date: 11 May 2022

( In partnership with imoney )

When we think of retirement, what is the first thing that comes to mind?

For many of us, we want to live how we want; no longer tied to the demands of a job. We want to sit back, relax, and spend our hard-earned savings living the life we did not have the time for while building our careers. While we would ideally like to enjoy our retirement in such a carefree manner, the reality is that retirement might also bring with it its own fair share of worries and anxiety. The biggest worry is the very real threat of not having enough saved up to pursue one’s aspirations for retirement.

Remember, it’s not just a few years that you need to support yourself after you retire, the actual number is at least 15 years. The average life expectancy in Malaysia is 75.6 years, so if you retire at the official retirement age of 60, that means you need to have enough money saved to maintain your retirement lifestyle for at least 15 years.

What about EPF savings?

You might already be familiar with the Employee Provident Fund (EPF). Because it is compulsory for employees and employers to contribute to this fund, many might think that this is more than enough to secure their future retirement lifestyle. However, according to the Ministry of Finance, only about 27% of active contributors to the EPF aged 18-55 are expected to have savings in their Account 1 that exceed the basic savings quantum stipulated according to age. For reference, the amount of recommended savings that individuals should have is around RM240,000 by age 55. The cost of living today is not the same as 20 years ago. As such, it is understandable why people would want to dip into their retirement savings to help get by, especially among those who had been adversely affected by the pandemic. As a result, their retirement fund risk being depleted, and financial plans have taken a back seat. While we navigate through these challenging times, it is important to refrain from withdrawing savings, if you don’t need to.

In fact, 48% of members now have savings in their EPF accounts after the series of special withdrawals allowed in recent years. While this may relieve some of the financial hardships that people are currently facing, they will risk facing more financial difficulties when they retire. At present, the number of senior citizens who need government aid is expected to increase from 3.5 million in 2021 to 5.3 million by 2030. This number will further grow to 7.4 million by 2041. Government assistance for such a huge number of people will likely focus on providing the minimum basic amount and will most certainly not be enough to maintain your ideal retirement lifestyle.

.

What can you do to build enough retirement savings?

Today, Malaysia’s 30% income replacement ratio is lower than the world average. The recommended minimum replacement rate is 70%, which means there is a big gap between what Malaysians are saving for retirement and how much money is actually needed. At an individual level, this means having to make up for the shortage by figuring out how much you really need. One important step to remember is to forecast the amount you need to retire comfortably. According to EPF’s Belanjawanku expenditure guide, an elderly couple living in the Klang Valley needs RM3,090 a month for a “reasonable standard of living” in 2019. Another thing to consider is the age you plan to retire. While the official retirement age is 60, you should adjust your retirement budget forecast if you want to retire earlier or later.

Here’s an example of how to calculate a retirement budget.

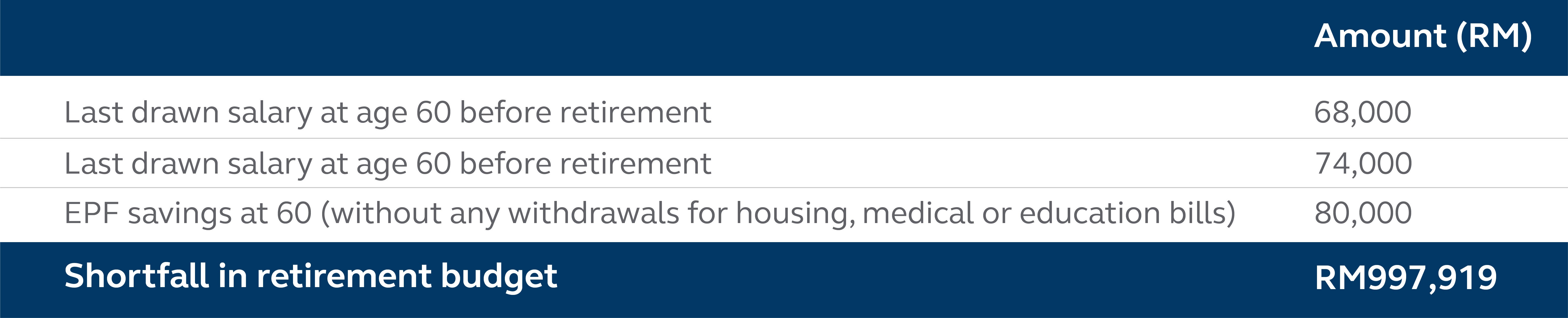

Salmah is a 22-year-old graduate earning RM2,500 monthly salary now and plans to retire at 60 years old with enough savings to last 20 years. Assuming she earns a 3% annual salary increase until she retires at 60, Salmah will have approximately RM974,641 worth of savings in her EPF account, assuming no withdrawals have been made. As such, she will be short of about RM997,919 if she intends to maintain her lifestyle for 20 years in retirement.

Clearly, saving for a stress-free retirement is something that everyone should take into consideration at an early stage! A useful guide to start saving is using the 60/20/20 rule. It is a simple budgeting strategy that helps you allocate your monthly income without breaking the bank. In this method, 60% of your monthly income goes to monthly living expenses including paying fixed bills. These can include things such as housing, utility bills, insurance, transport, food, credit card bills etc. An additional 20% of your monthly income should be dedicated to emergency savings for unexpected events such as car breakdown, rooftop leakage, sudden loss of income, medical expenses, among others. The final 20% can be used to invest in your long-term or short-term goals such as travel, umrah, retirement or anything else that enriches your lifestyle. This budget gives you the flexibility to generate extra income while ensuring you’re making saving a priority.

Consider investing now to earn income during retirement

Apart from saving up enough for your retirement fund, another way you can help augment and enjoy your retirement years is to ensure that you have a form of income post-retirement. While some might prefer to keep active and work a part-time job after retirement, others might want to consider turning their hobbies and interests into their source of income. For example, someone who enjoys baking could probably sell made-to-order pastries and confectioneries. If you prefer a more passive source of income, you might want to consider investments that have good potential for returns.

- Unit Trusts – A unit trust is essentially a pool of money that is collectively managed by a fund manager. Your money will be pooled with that of other investors and invested in a diversified portfolio to achieve the trusts’ investment objectives. The biggest advantages that unit trusts offer are that they are simple, do not require too much knowledge to invest in, usually require a low initial investment, possess high liquidity, and are often managed by a team of professionals who are actively managing your portfolio.

Principal offers a selection of over 70 unit trust funds for investors based on their risk tolerance and length of time available.

- Private Retirement Schemes (PRS) – These are voluntary long-term savings and investment schemes that are designed to assist you in saving more for retirement. In a way, it is essentially another form of EPF that can help supplement your retirement savings. These schemes are safe, flexible, and regulated, providing a hefty safety net for those seeking to complement their EPF and retirement savings

You can invest in Principal PRS funds by enrolling online using the Private Retirement Scheme platform or through Principal consultants.

What Principal can do to help you achieve your retirement lifestyle

The earlier you start preparing, the easier time you will have in securing sufficient funds for your eventual retirement. Rather than worrying if your retirement funds will be enough, proper preparation and execution can lead to your golden years being just as fulfilling as your pre-retirement life.

If you ever need assistance in building your long-term road map to financial success, Principal Asset Management has got you covered. For those aged 55 years and above, Principal has recently launched their PRS decumulation solution: Principal RetireEasy Income fund and Principal Islamic RetireEasy Income fund.

Benefits of the Principal PRS decumulation solution:

- It comes with Regular Withdrawal Plan (RWP) for monthly, quarterly, semi-annual, or annual payments

- Customise your post-retirement cash flow based on your available funds

Continue to invest your remaining balance in the funds for potential returns.

What to do next?

Start visualising your retirement days. If you need any assistance, consider reaching out to a financial consultant. (We can help you find one.) They can help you discover your goals and advice you based on your risk tolerance.

In the meantime, here’s what you can read on how to:

- to supplement your retirement savings with Private Retirement Scheme (PRS).

- diversify your EPF savings via EPF’s i-Invest.

Disclaimer

You are advised to read and understand the relevant Prospectus, Information Memorandum and/or Disclosure Document including any supplemental thereof and the Product Highlight Sheet (if any) before Investing. Among others, you should consider the fees and charges involved. The registration of the relevant Prospectus, Information Memorandum and/or Disclosure Document including any supplemental thereof and the Product Highlight Sheet (if any) with the Securities Commission Malaysia (SC) does not amount to nor indicate that the SC recommends or endorses the funds. A copy of the relevant Prospectus, Information Memorandum and/or Disclosure Document including any supplemental thereof and the Product Highlight Sheet (if any) may be obtained at our offices, distributors or our website at www.principal.com.my. The issuance of any units to which the relevant Prospectus, Information Memorandum and/or Disclosure Document relates will only be made on receipt of an application referred to in and accompanying a copy of the relevant Prospectus, Information Memorandum and/or Disclosure Document. Please be advised that investment in the relevant unit trust funds, wholesale funds and/ or private retirement scheme carry risk. An outline of the various risk involved are described in the relevant Prospectus, Information Memorandum and/or Disclosure Document. As an investor you should make your own risk assessment and seek professional advice, where necessary. Securities Commission Malaysia does not review advertisements produced by Principal.