MARKET COMMENTARY

September 2025

Global Outlook

In August 2025, global equity markets rallied for the fourth month. The largest gainers were Indonesia, Malaysia, and Japan, at 4.6%, 4.1%, and 4%, respectively. Korea, India, and Thailand dipped 1.8%, 1.7%, and 0.5%, respectively. Bond indices performances ranged from -1.5% to +0.8%.1

The Fed maintained the Fed Fund rate at 4.50% during the July 2025 FOMC meeting. The Fed guided that the uncertainties from the proposed tariffs do not provide leeway for rate adjustments. The ECB maintained the interest rate at 2.00% during the July 2025 meeting.

We prefer Equity over Cash in Asia. Markets are focusing on easing monetary conditions with more fiscal spending and a healthy risk appetite. Prefer companies with strong free cash flows, visible growth, yields and unique drivers. We favour financials (stock exchanges, brokers, life insurance), new consumption (digital services, culture and lifestyle), industrials (defence, nuclear, power equipment) and technology (platform tech, semicon).

Global Outlook of the two capital markets: Fixed Income & Equities

Region: Developed economies

Fixed income

- Our view: Positive.

- The Fed maintained the Fed Fund rate at 4.50% during the July 2025 FOMC meeting. The Fed guided that the uncertainties from the proposed tariffs do not provide leeway for rate adjustments.4

- We will take some profit on some corporate bonds with rich valuation post the rally but maintain an overweight position. Maintain some tactical positions in the government bonds with a bias towards higher weight, in lieu of the rising expectation of a rate cut in the September FOMC meeting.5

Equity

- Our view: Positive.

- The Fed maintained the Fed Fund rate at 4.50% during the July 2025 FOMC meeting. The Fed guided that the uncertainties from the proposed tariffs do not provide leeway for rate adjustments.4

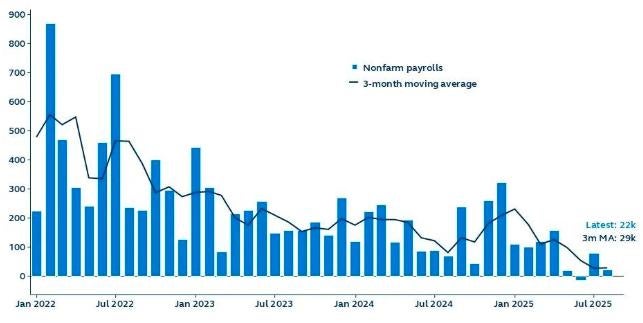

- Slight Overweight for the US and Neutral on the EU and Japan. Higher off-benchmark exposure, including Asian stocks. With the weaker July and Aug payroll data and downward revisions to prior months, expectations for a September rate cut have increased.

Region: Regional (Asia-Pacific ex-Japan)

Fixed income

- Our view: Positive.

- Pockets of opportunity in local currency Asian and Chinese credits, as yields remained relatively attractive.6

- We expect investment-grade Asian bonds to provide a gross yield of 5.50% to 6.00% in 2025.6

Equity

- Our view: Positive.

- We prefer Equity in Asia. While tariffs are higher than 10% after negotiation, markets are focused on easing financial conditions with more fiscal spending, easier monetary policy and stable/falling inflation.

- Like companies with strong cash flows, visible growth, yields and unique drivers. Favour financials, new consumption (digital services and lifestyle), industrials (defence, nuclear, power equipment) and technology.3

Region: China

Fixed income

- Our view: Neutral.

- Net credit bond supply in July 2025 rose to RMB778bn from RMB418bn previously. This came from issuances from financials and SoEs. LGFVs saw net redemption of RMB42bn.

- The default rate for July 2025 remained at 0.10% as per June 2025.

Equity

- Our view: Neutral.

- Prefer domestic-oriented companies with growth and strong cash flow. Like selected names in technology, domestic consumption, infrastructure, communications and financials.

- Manufacturing PMI for Aug 2025 rose to 49.4 from 49.3 previously. The Services PMI rose to 50.3 from 50.1 over the same period.9

Region: Domestic (Malaysia)

Fixed income

- Our view. Positive.

- BNM cut the OPR to 2.75% during the July 2025 MPC meeting. The reduction in the OPR is a pre-emptive measure aimed at preserving Malaysia’s steady growth path amid moderate inflation prospects.10

- To take profit on government bonds while maintaining tactical positions in anticipation of the upcoming maturities. With widening credit spreads, we prefer the corporate segment for better total return.3

Equity

- Our view: Positive.

- The National Energy Transition Roadmap (NETR) and the Industrial Master Plan 2030 would revitalise domestic investment and buoy consumption.3

- Pairing high-dividend, big-cap, defensive stocks with exposure to growth companies, either with domestic-focused demand or exposed to the structural growth of technology. Pockets of opportunities in Construction, Utilities and selective Banks.

Investment Implication:3

- Global: Slight Overweight U.S., Neutral Europe & Japan and Underweight Cash. While the Trump administration's policy remained a primary driver, there is less uncertainty compared to three months ago. The U.S. economy is likely to slow down, and the risk of recession appears low. Policy shifts could promote growth with promises of U.S. deregulation, and tax policy may provide a boost to the U.S. economic outlook. With the Trump tax bill approved on July 4th, the market will turn its attention to economic data and observe the strength of the labour market for further direction. U.S. valuations are elevated, but resilient earnings and low recession risk support a gradual re-risking. Europe's fundamentals remain weak despite recent policy reform. Germany's fiscal overhaul is expected to be supportive for long-term growth; however, recent market price action appears to have moved ahead of fundamentals, and in the near term, we see limited positive catalysts to sustain the momentum.

- Malaysian Equity: Continue to advocate a barbell strategy, given the current uncertain global environment, where near-term volatility is expected to continue, mainly due to the US administration’s unpredictability. Concerns over a tariff-driven worldwide slowdown and the constant changes to Trump’s trade policies could weigh on market confidence and pressure Malaysia’s growth and earnings outlook. That said, downside risks may be partially cushioned by the recent supportive domestic-driven initiatives by the government. The barbell strategy is pairing high-dividend, big-cap, defensive stocks with selective exposure to growth companies with domestically focused demand. We believe there are still pockets of opportunities to invest, especially in sectors such as Construction, Property, Utilities and selective Banks. Key risks include a further escalation of global trade tensions affecting business and investment conditions.

- Malaysia Fixed Income: After the recent rally on the back of the OPR cut, the local bond market has stabilised with profit takers emerging, looking to lock in gains given a resilient growth target and some stability on the trade tariff front. We look to take profit on government bonds while maintaining tactical positions in anticipation of the upcoming maturities. With widening credit spreads, our preference remains in the corporate segment for better total return. We continue to take profit on the overvalued credits and rotate to primary issuances.

- Trade headlines are likely to stay top of mind for investors. One reason markets have appeared to be taking Trump’s tariff threats in stride is the recognition of a still resilient U.S. economy and expectation that the Federal Reserve will resume policy easing next month. We maintain that the rationale for investing in both Equity and Fixed Income remains strong, and we still foresee additional growth in the coming years.

- We reiterate the importance of keeping sight of longer-term investing principles that can boost risk-adjusted rates of return through portfolio diversification and an emphasis on quality growth and income to navigate the volatility ahead. Our strategy has also emphasised focusing on companies that demonstrate the attributes of large-cap defensiveness, with earnings that are more domestically focused. Additionally, quality bonds have historically offered portfolio stability, especially in times of uncertainty.

- We remain a slight preference for equities over fixed income. Key themes for 2025 include: i) the U.S. economic outlook and the narrative surrounding potential rate cut by the U.S. Federal Reserve; ii) capital movements towards Asia; and iii) the impact of tariffs and geopolitical risks on asset valuations.

Special Topic3:

After the recent weak payroll print, a June contraction, and four consecutive months of sub-100,000 gains, a September rate cut is virtually guaranteed. The focus will now likely shift to the magnitude of the cut and the potential for additional reductions. While markets might see a September rate cut as a proactive measure, any further deterioration in the labour market could swiftly change the narrative from viewing rate cuts as stimulative to seeing them as a response to a faltering economy. Recession is still not our base case.

Glossary:

UW: Underweight

OW: Overweight

MoM: Month-over-Month

YoY: Year-over-Year

FOMC: Federal Open Market Committee

ECB: European Central Bank

UST: United States Treasury

PMI: Purchasing Managers Index

SoE: State-Owned Enterprise

SEZ: Special Economic Zone

BNM: Bank Negara Malaysia

MPC: Monetary Policy Committee

Disclaimer

Past performance does not guarantee future results. Performance data represents the combined income and capital return as a result of holding units in the Fund for the specified length of time, based on bid-to-bid prices. Earnings are assumed to be reinvested.

Sources :

- Bloomberg, 31 July 2025

- Federal Reserve Board, 31 July 2025

- Principal, 31 July 2025

- European Central Bank, 31 July 2025

- Federal Open Market Committee (FOMC), 31 July 2025

- JP Morgan Research, 31 July 2025

- Bloomberg, 31 July 2025

- BofA Securities, 31 July 2025

- National Bureau of Statistics of China, 31 July 2025

- Bank Negara Malaysia, 31 July 2025